Soundmark Wealth Management by the Numbers

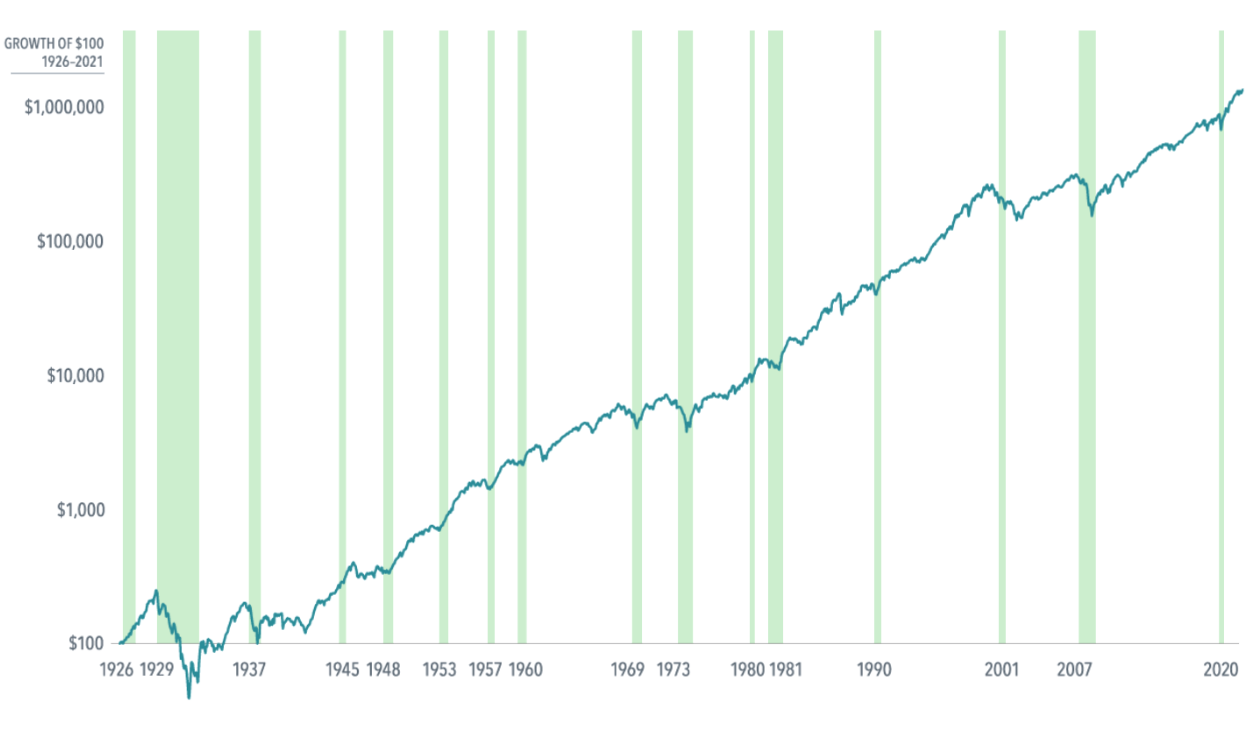

Our firm combines a common-sense investment philosophy with a straightforward approach to financial planning that allows you to do just that—focus on your life and ignore Wall Street.

Our firm combines a common-sense investment philosophy with a straightforward approach to financial planning that allows you to do just that—focus on your life and ignore Wall Street.

With the passing of the SECURE Act 2.0, we are sharing a few of the legislative highlights that may play an important role in your financial plans.

The SECURE 2.0 Act of 2022 has a new provision which could make it easier to preserve the tax-free status of unused funds in 529 plans.